When you mine Bitcoin, you’re not just running machines-you’re running a business. And like any business, the IRS wants its share. The moment your mining rig solves a block and you receive that new Bitcoin, Bitcoin mining taxes kick in. Not when you sell. Not when you cash out. Right then. At that exact second. That’s the rule. And if you don’t track it, you’re risking penalties, audits, or worse.

Bitcoin Mining Income Is Ordinary Income-Not Capital Gains

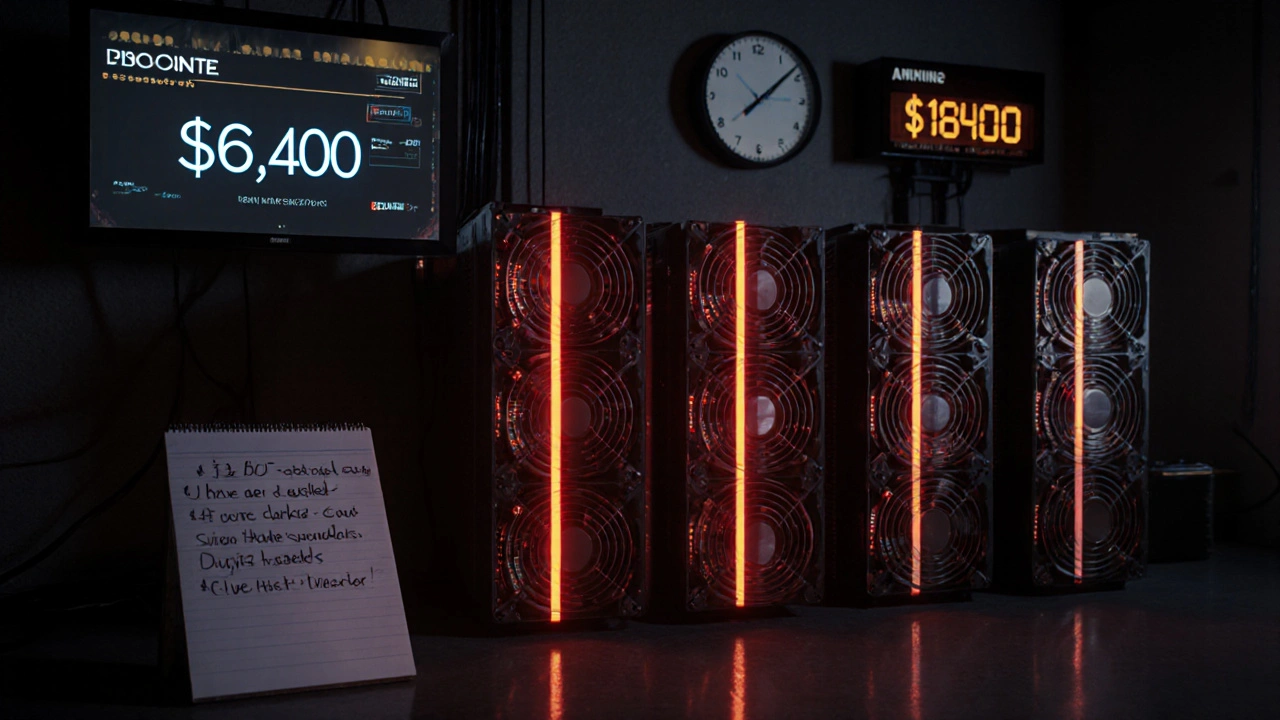

The IRS doesn’t treat Bitcoin like cash. It treats it like property. That means every Bitcoin you mine is taxable income the second it lands in your wallet. The amount you report? The fair market value in U.S. dollars at the exact time you received it.Let’s say you mined 0.15 BTC on April 3, 2024, at 14:07:22 UTC. The price of Bitcoin that second was $68,400. Your taxable income? $10,260. Doesn’t matter if you never sold it. Doesn’t matter if you still have it in cold storage. You owe tax on that $10,260 as ordinary income.

This isn’t speculation. It’s IRS guidance from Notice 2014-21 and clarified in Chief Counsel Advice 2019-001. The IRS has been enforcing this since 2016 with subpoenas to Coinbase and other exchanges. In 2023, IRS Commissioner Danny Werfel said it plainly: "Virtual currency received from mining is taxable income at its fair market value on the date of receipt."

Compare this to trading. If you buy Bitcoin and sell it later, you pay capital gains tax-maybe 0%, 15%, or 20% if you held it over a year. But mining? No holding period matters. You pay your regular income tax rate-between 10% and 37% federally-plus 15.3% self-employment tax if you’re operating as a business.

Is Your Mining a Business or a Hobby? It Changes Everything

Here’s where most miners get tripped up. If you’re mining as a hobby-say, you run one Antminer in your garage on weekends-you report income on Schedule 1. But you can’t deduct any expenses. No electricity. No hardware. Nothing.If you’re running this like a business-multiple rigs, dedicated space, consistent operation, profit motive-you file Schedule C. Now you can deduct everything: electricity, internet, cooling, pool fees, even the cost of your mining rig.

The IRS uses nine factors to decide if it’s a business. Do you do it regularly? Do you keep records? Do you spend time optimizing your setup? Do you have a plan to turn a profit? If yes, you’re likely a business. And if you’re a business, you can take advantage of Section 179 and MACRS depreciation.

Depreciate Your ASIC Miners-Don’t Just Write Them Off

A top-end ASIC miner like the Antminer S19j Pro costs $3,500-$5,000. You can’t just deduct the full cost in one year unless you use Section 179.Section 179 lets you deduct the full cost of qualifying equipment in the year you put it into service-up to $1,160,000 in 2024. But there’s a catch: your total deduction can’t exceed your net business income. If you mine $8,000 this year and buy a $10,000 rig, you can only deduct $8,000 under Section 179. The rest rolls over to future years.

Or you can use MACRS depreciation. ASIC miners fall under the 5-year property class. That means you deduct 20% per year over five years. But here’s the kicker: if you bought your miner between September 28, 2017, and December 31, 2024, you can also take bonus depreciation. In 2024, that’s 60%. So if you buy a $4,000 miner in 2024, you can deduct $2,400 right away (60%) plus $800 under Section 179 (if you have income to cover it), leaving $800 to depreciate over the next five years.

Most professional miners use a mix: Section 179 for smaller rigs, MACRS for larger ones. But you have to elect it on Form 4562. Don’t skip this. If you don’t, you lose the deduction.

Record-Keeping: The IRS Expects a Digital Ledger-Not a Notebook

You can’t just say, "I mined 5 BTC last year." The IRS wants proof. Every single time you receive a reward, you need:- Date and time (to the second) the Bitcoin was received

- Exact fair market value in USD at that moment

- Blockchain transaction hash

- Wallet address that received it

- Amount of pool fees paid (if applicable)

Some miners get 10-20 rewards a day. That’s hundreds of entries per year. Manually tracking this is a nightmare. Most use crypto tax software like CoinLedger, TokenTax, or Koinly. These tools connect to your mining pool via API and auto-import every payout. They pull live Bitcoin prices from CoinGecko or CoinMarketCap and calculate your income for each event.

One miner on Reddit said he had 347 mining events in 2023. He spent 17 hours manually entering them before switching to software. It took 45 minutes after that.

Don’t forget to save receipts for your hardware. The IRS doesn’t ask for them upfront-but if you’re audited, you have to prove you bought it. Keep purchase invoices, shipping labels, and specs. Hold them for at least seven years. That’s the recommended window for businesses claiming deductions.

Electricity Costs: The Biggest Deduction (and the Hardest to Track)

Electricity is your largest operating expense. If you’re a business, you can deduct it. But here’s the problem: your miner isn’t the only thing using power. Your lights, fridge, and TV are too.The IRS allows you to allocate electricity costs based on wattage. If your miner draws 3,200 watts and your whole house uses 12,000 watts total, you can deduct 26.7% of your electricity bill as a business expense. You need to track your usage over time-some use smart plugs with energy monitoring apps.

Don’t just guess. The IRS has rejected claims where miners said "half my bill" went to mining. Be precise. Take screenshots of your power meter before and after a week of mining. Log your rig’s wattage. Use a tool like PowerCalc or Hashrate Monitor to track real-time draw.

Pool Fees Are Deductible-But Most Miners Forget

Mining pools charge fees-usually 1-3% of your reward. These are not "losses." They’re business expenses. The IRS says so in Publication 535. You can deduct them as ordinary and necessary costs of running your mining operation.Yet TurboTax support data shows 38% of mining-related help tickets in early 2024 were about misreported pool fees. Some miners subtract them from their income. Others ignore them. Both are wrong. You report your full mining reward as income, then deduct the pool fee as an expense. That’s two lines on Schedule C: one for income, one for expense.

What Happens When You Sell Your Mined Bitcoin?

When you finally sell, you pay capital gains tax. But the cost basis isn’t what you paid for the rig. It’s what you reported as income when you mined it.Example: You mined 0.5 BTC in January 2024 at $42,000/BTC. You reported $21,000 as income. Later, you sell that 0.5 BTC in June 2025 for $70,000/BTC. Your capital gain? $35,000 - $21,000 = $14,000. You pay long-term capital gains tax on that $14,000 because you held it over a year.

That’s not double taxation. That’s two separate events: income tax at receipt, capital gains tax at sale. The American Institute of CPAs confirmed this in Technical Questions and Answers #5200.02. Your cost basis is always the FMV at mining.

What If You’re Not in the U.S.?

This article covers U.S. tax law. If you’re outside the U.S., rules vary. Canada treats mining as business income. The UK taxes it as miscellaneous income. Australia treats it as ordinary income and allows depreciation of equipment. But if you’re a U.S. citizen or resident-even if you live abroad-you still owe U.S. taxes on worldwide income.Don’t assume your local rules override IRS rules. If you’re a U.S. taxpayer, the IRS wins.

Common Mistakes That Trigger Audits

- Not reporting mining income at all

- Using the wrong FMV (e.g., average price for the day instead of exact time of receipt)

- Claiming equipment depreciation without Form 4562

- Forgetting to deduct pool fees

- Using personal electricity bills without allocation

- Not keeping transaction hashes or timestamps

The IRS uses blockchain analytics firms like Chainalysis to trace crypto flows. They’re not guessing. They’re matching wallet addresses to exchange accounts. If your wallet sent BTC to Coinbase and you didn’t report the mining income, they’ll find it.

Next Steps: What to Do Right Now

- If you mined in 2024: Gather all your mining payouts. Use CoinLedger or Koinly to auto-import them.

- Calculate your total mining income. Add up the FMV of each reward.

- Collect receipts for all mining hardware purchased in 2024.

- Calculate your electricity allocation using wattage or smart meter data.

- Decide: Section 179 or MACRS? If you’re unsure, talk to a crypto-savvy CPA.

- Start logging every future mining event-date, time, hash, value, wallet.

Don’t wait until tax season. The sooner you set up your system, the less stress you’ll have. The IRS isn’t going away. And they’re getting better at tracking crypto. If you’re mining, you’re in the system. Make sure you’re reporting correctly-or you’ll pay the price later.

Do I have to pay taxes on Bitcoin mining even if I don’t sell it?

Yes. The IRS treats mined Bitcoin as income the moment it’s received. You pay ordinary income tax on its fair market value at that exact time, regardless of whether you sell it later. Not selling it doesn’t make the tax disappear.

Can I deduct my electricity bill for Bitcoin mining?

Yes-if you’re operating as a business. You can deduct the portion of your electricity bill used for mining. The IRS accepts reasonable methods like calculating based on your miner’s wattage compared to your total home usage. Keep logs and calculations to support your claim.

What’s the difference between Section 179 and MACRS depreciation?

Section 179 lets you deduct the full cost of your mining equipment in the year you buy it, up to $1,160,000 in 2024. MACRS spreads the deduction over five years at 20% per year. You can also take 60% bonus depreciation in 2024 on top of either method. Section 179 gives you a bigger upfront deduction, but only if you have enough taxable income to use it.

Are mining pool fees tax-deductible?

Yes. Pool fees are considered ordinary and necessary business expenses under IRS Publication 535. You report your full mining reward as income, then deduct the pool fee as a separate expense on Schedule C. Don’t reduce your income by the fee amount-deduct it separately.

What happens if I don’t report my mining income?

The IRS can audit you and assess back taxes, penalties, and interest. For willful evasion, penalties can include up to $250,000 in fines and five years in prison. With blockchain tracking tools like Chainalysis, the IRS can match your wallet addresses to exchange accounts. Ignorance isn’t a defense.

Do I need to report mining income if I only made $1,000?

Yes. There’s no minimum threshold for reporting cryptocurrency income. Even $1 of mining income must be reported. The IRS doesn’t care how small it is-your obligation to report it remains.

Can I use crypto tax software to file my mining taxes?

Yes. Tools like CoinLedger, Koinly, and TokenTax are designed specifically for crypto miners. They auto-import data from mining pools, calculate FMV per transaction, track depreciation, and generate Schedule C and Form 4562. Many CPAs recommend them for accuracy and time savings.

15 Responses

Ugh I just mined 0.02 BTC and now I gotta file Form 4562? This is why I quit crypto. All that power just to pay the government more money. I could’ve just bought a fucking pizza instead.

Actually, the IRS guidance is clear: mining income is ordinary income at FMV on receipt. Section 179 applies only if you’re operating as a business, not a hobby. You need to document everything. No guessing.

Let me guess-you’re one of those guys who thinks the IRS gives a damn about your Antminer S19j. Wake up. The IRS doesn’t care about your 2024 mining rig. They care about your Coinbase account. And if you didn’t report the $10k you turned into cash last year, you’re already in trouble. Stop overcomplicating it.

It is imperative to note, with the utmost clarity, that the Internal Revenue Service’s position on virtual currency-as articulated in Notice 2014-21, and reaffirmed in Chief Counsel Advice 2019-001-is unequivocal: the moment of receipt constitutes a taxable event. Failure to report the fair market value at the precise second of block reward confirmation constitutes a material omission under Section 6038, and may trigger penalties under Section 6662. The notion that one can avoid taxation by merely holding the asset is not only legally untenable, but also demonstrably erroneous.

Okay but like… I mined 12 times yesterday and I didn’t even know I was supposed to track the exact second? I thought it was just the day?? I’m so behind. I just used CoinLedger and it pulled in all my pool payouts with timestamps and prices?? I cried. Like, actually cried. This is the most stressful thing I’ve ever done and I once did taxes while crying over a breakup.

Hey new miners! Don’t panic! Use Koinly or CoinLedger-they connect to your pool via API and auto-import every payout. No manual entry. Just click, verify, and boom-you’ve got your Schedule C ready. Also, save your ASIC receipts. I lost mine once and spent 3 weeks digging through Amazon order history. Don’t be me. You got this 💪

My friend, you must understand that the Internal Revenue Service requires documentation for all forms of income, including cryptocurrency derived from mining activities. One must maintain accurate records, including transaction hashes, timestamps, and fair market values. It is not optional. It is the law.

Let me tell you something about the IRS-they’ve been tracking crypto since 2016. They have blockchain analytics contracts with Chainalysis, Elliptic, and CipherTrace. They’re not waiting for you to file. They’re cross-referencing wallet addresses with KYC’d exchanges. If you mined $10k in 2023 and didn’t report it, they already have your name, your SSN, your address, and your dog’s name. You think you’re hiding? You’re not. You’re just building a case against yourself. And when they come for you, you’ll be begging for an offer in compromise. Start documenting. Now.

Guys, I get it-this is overwhelming. But you don’t have to do it alone. Talk to a crypto CPA. They’re not expensive. And honestly, if you’re mining seriously, you’re already making more than their fee. Save yourself the stress. Set up your tracking now. You’ll thank yourself in April.

While the article presents a compelling argument regarding the tax implications of Bitcoin mining, one must question the ethical underpinnings of incentivizing such energy-intensive activity through fiscal leniency. Is it truly prudent to allow deductions for electricity consumption that may contribute to environmental degradation? The IRS, in its wisdom, ought to consider broader societal costs.

They say the IRS tracks everything, but what if they’re lying? What if Chainalysis is just a front for the Federal Reserve to control crypto? I’ve read forums where people say the IRS doesn’t even have access to the blockchain-only the exchanges. So if you mine to a non-KYC wallet, and never touch an exchange, you’re safe. Right? Or is this all a trap? I’ve started mining in my basement with a Faraday cage. I don’t even have Wi-Fi. I’m using a USB drive to transfer hashes manually. I’m the only one who knows what I’m doing.

There’s something deeply human about this whole thing. We’re building a new kind of economy, and the government is trying to fit it into old boxes-ordinary income, depreciation schedules, tax forms from the 1950s. But Bitcoin mining isn’t just accounting. It’s physics. It’s electricity. It’s time. It’s the cost of keeping a decentralized ledger alive. The IRS wants to tax the output, but they don’t want to understand the process. Maybe the real tax isn’t the money-it’s the exhaustion of trying to explain it to someone who doesn’t care to listen.

Right, so the Yanks think they own the world’s tax rules now? I mine in the UK and we don’t even call it income-just miscellaneous. But if you’re a US citizen living in London, you still gotta report? That’s insane. You’re taxing people twice-once for living here, once for mining. And don’t even get me started on the electricity allocation nonsense. Who the hell calculates wattage for their fridge vs their ASIC? This is why I’m moving to Portugal.

So you’re telling me I have to track every single mining reward to the second… but the IRS doesn’t care if I use a 20-year-old laptop to do it? You’re not serious. This is why crypto will die. It’s not regulation-it’s bureaucratic torture. And you people are actually proud of this? Pathetic.

Just a quick note: if you’re using MACRS depreciation on your ASICs, remember to file Form 4562 with your return. I missed it last year and had to amend. Took 3 months. Also, bonus depreciation is a gift-don’t sleep on it. 🙌 And yes, pool fees are deductible. I’ve seen too many people mess this up. You’re not reducing income-you’re adding an expense. Simple. Clean. ✅